Money is a strange thing; it behaves in weird ways. And the more you uncover its mechanics, the stranger it becomes, and your intuitions deceive you. This post will give you a sneak peek into this world and show how your common sense works against you.

The post contains lots of loose ends for you to tie up. Think and reason, and the answers will appear.

Here is the first one. As you read, ponder this question: is this behavior you are seeing designed or emerged?

The more you have, the better

As you look around, the world agrees with you. More money is better, says your common sense. This belief is so strong that people set goals to pile up some cash. There is also the common saying that “money attracts money”. The Bible seems to agree.

“For everyone who has will be given more, and he will have an abundance. But the one who does not have, even what he has, will be taken away from him.” – Matthew 25:29

I want to challenge this perception. What you are experiencing is not due to the abundance of money but your actions. Owning more of this fictional item will give you more opportunities. However, let’s set that aside for now and focus solely on the possession of it. That’s money in your pocket (cash) and liquidity at your bank (debit balance). The fact that you can spend money doesn’t change the point I will make, so you can safely ignore that.

Money is changing

Jane has $100.000 in her bank account, while John has $30.000. Jane’s ahead $70.000; that’s pretty clear. Common sense suggests that the advantage and size should hold over time, given that nothing else changes. But money is peculiar and isn’t constant. It loses its value due to inflation, which we’ll get to shortly.

Let’s see what happens to our heroes over time.

The more you have, the greater your losses over time.

Wait a second, if neither of our heroes spent the money, then after 50 years, Jane’s still at $100.000 and John’s at $30.000. What’s that dissolving magic you did there?

Good question. You start to feel something fishy here. And indeed, there is; it’s the difference of value and price.

The price of value

Lots of times, these terms are used interchangeably. In some countries, even the accounting law mixes them up.

Coincidence? 🧐

Accounting is strange in its own right, as it works with prices over potentially significant timeframes. While the numerical representation of fees can be compared, added, and subtracted, it completely misses the value of those costs.

Price and value are far from being equal. Price is the amount of money one must give in exchange for a good. Value, conversely, represents the worth or utility we assign to a good.

What’s the intrinsic value of a $100 bill?

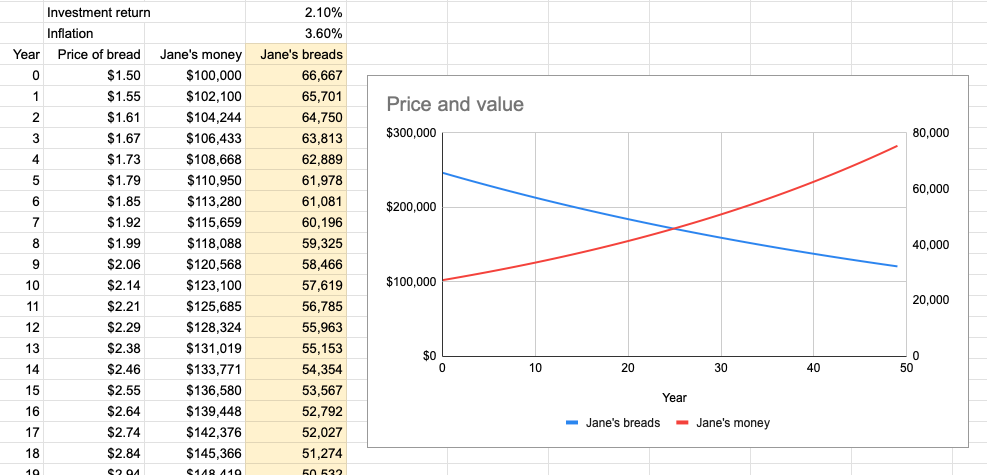

Let’s adjust our previous graphs to account for this. We’ll measure price in dollars and value in the number of breads our money can buy.

This warrants a bit more explanation. The price of $1 at any given time is $1. Its price is constant. Hence, the horizontal line shows how much money Jane and John have. The amount of money each possesses does not change over time.

The value of a loaf of bread is precisely one loaf of bread (or 3 eggs, for that matter) at any given time. Its value is constant; it provides the same amount of nutrients, and given our physiology doesn’t change much, it is equally valuable to humans now and in the future. However, the price of bread isn’t static; it increases over time.

It’s crucial to understand the difference. Be very careful when the value of something is expressed as a price tag. Especially if time is in the picture.

Don’t mistake the above arguments with the net present value (NPV) concept, where you discount future promises to their current worth. In our examples, we are not discounting future money; we simply look at its value and price in the future.

Also, humans are sentimental enough to attach imaginary value to things. It is possible for something to have a high value without having much utility. Think artwork. You could argue that it’s not value but price tags, and I wouldn’t dispute it. What’s important is that our use case above doesn’t deal with imaginary prices or values. No “holy bread”.

How would you rate gold in terms of value and price?

Of course, value is subjective, as is the price someone is willing to pay. The above arguments still hold.

Money loses its value (purchasing power) over time. This loss is drastic over long periods because of the exponential decay or under extreme conditions (like hyperinflation).

Is this always true? What exceptions can you think of?

Money is conjured ehm printed

As you progress through life, there is a point when you first meet inflation. Someone may tell you, or you may experience it firsthand. After this encounter, your rational self understands what’s happening, but it most likely will not become an integral part of your thinking. Therefore, even if you know this is the case, you won’t take too much action to counter it. And this will ultimately make you a loser. It’s hard to accept this reality, especially when your bank account doesn’t seem to agree. After all, you have more money!

It is possible to have more money (price) and still realize less value (purchasing power). Consider the following graphs.

Guess which number is shown to you every time you look at your balance 😱. It would look very different if you were to track your money by its value. I suggest you start doing that. You might well be in for some surprises.

You can explore the current inflation levels here. Typically, inflation between 2-4% is considered healthy.

Why? And says who?

Okay, so money loses value over time, and to some extent, the world considers this normal. But what’s driving inflation? Do people automatically devalue their money even though they probably don’t want to?

Wouldn’t that be great psychological programming? 🧐

The answer is more straightforward. Although it requires many humans to act similarly to a stimulus. You probably heard this concept before; it’s supply and demand. The more there is of something, the cheaper it becomes; its price is decreasing. Its value does not. A ton of bread does not affect the nutrients a single loaf provides. Its price, however, will get lower as it is effortless to obtain.

With money, it’s more tricky. As more money enters the system, the demand for goods and services will increase. Simply because more people can afford them. As demand grows, so does the price tag. This is the ultimate cause of your money losing its value. Because of the competition, you’ll be able to purchase less goods for the same amount of money. If everyone has more, nobody’s ahead. These dynamics will, over time, stabilize the prices at a higher point than before new money entered the system.

New money entering the system

In most countries and economic regions (EU), the issuance of new money is in the hands of a central bank. Their primary aim is price stability. They reach this by carefully controlling inflation with various tools like adjusting interest rates, reserve requirements, and printing money.

If you want to get more into it, read the classic Modern Money Mechanics workbook and watch How The Economic Machine Works by Ray Dalio.

Are there other entities conjuring money out of thin air? Or is it just the central bank?

When money flows out of central banks, those already owning some are losers. The more significant your pile, the larger your loss. If your stack is empty, your loss is 0.

What happens when your money pile is negative; when you owe?

Yep, you are “gaining” value. The price you owe stays the same, but the value does not. It decreases.

Are you saying that inflation lowers the value of debt?

YES!

Owing money

There are many types of loans, from credit cards and mortgages to personal loans and business credit lines. There are differences, but the fundamentals are relatively similar in each case. An entity gives you money in the present and expects you to pay it back with a premium in the future. This premium is usually called interest. Depending on the construction, your installments typically contain interest and may include a principal. There is much more to credit and loans, but these basics are enough for the point I want to make.

Some food for thought: what are the most critical parts of a loan contract?

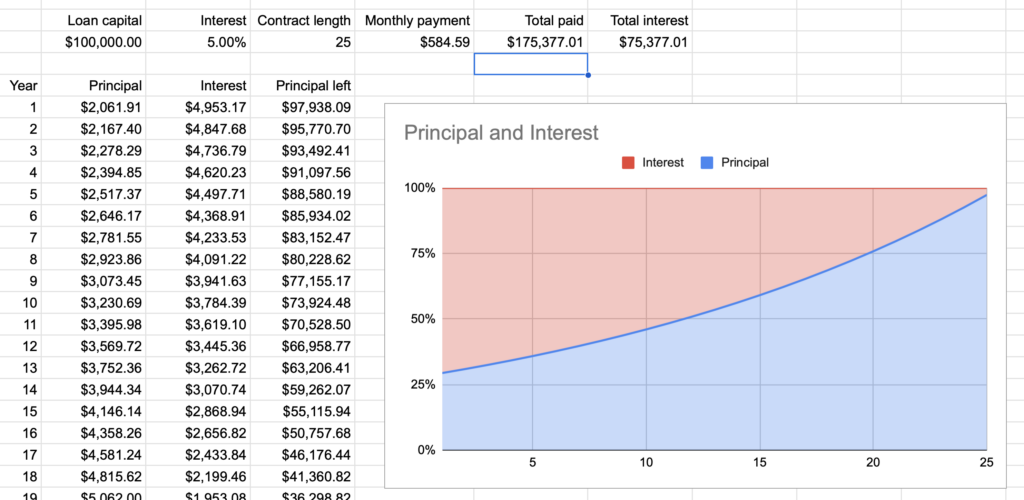

When you sign a credit contract, consider it an agreement of present and future transactions. Leave aside the classical “payback” concept, which will fall apart when discussing value instead of price. Let’s take a typical mortgage as our example.

John obtains $100.000 credit for some real estate. His contract is for 25 years with a fixed interest rate of 5%. That will be a monthly payment of ~$585 for 300 months. That will total $175.377 over the length of the contract. Of which, $100.000 is principal and $75.377 is interest. This construction is called an annuity loan or installment loan. John pays the same amount every month, and the ratio of principal and interest varies. Here’s a visualization.

Let’s see the same setup from the perspective of value. Value will be represented by purchasable breads with the given amount of money.

A normal 3% inflation will result in paying 50% less in value after 25 years. The cumulative interest on value is only 23.82%, while it is more than 75% on price. This is about ~1.65% value interest yearly. That’s 1.65% value vs. 5% price.

Interest usually follows the market, including inflation, with some lag. The remaining principal is never value-corrected throughout your loan term. And that’s the key.

Fascinating, isn’t it?

When inflation exceeds your interest, you are directly profiting from this construction. This can happen more often than you think, especially in a volatile economy. It’s not always free money, though. The above market forces are well-known by banks as well. And your interest is calculated accordingly. While you can realize profit by taking out mortgages and hoping for inflation to top your interests, there are better ways to get rich 🤑.

Takeaways

A couple lessons emerge from this. Not counting the “shoot for low interest rates” advice.

Think of scenarios when you owe money without paying any interest. Now, think about the opposite. Someone owing you without paying interest. Which is more common? 😳

Take this section with a grain of salt. It is definitely not financial advice. I invite you to apply what you have learned to your situation. Also, think outside the scope of classic loans and use these ideas more abstractly. Consider questions like: am I seeing value? How would that compare to a price? Am I working with prices or values?

1) Increase “borrowed capital”

The idea behind this is to expose yourself to the upside of inflation as much as possible while being safe. Given that you have good terms on your financing, it can provide investment opportunities. It is better to be ready for the option when it arises. What you do with the money is critical. Invest it wisely; otherwise, it’s just wasted.

And no, I am not advocating for taking on as much personal loan as you can. Instead, think critically when obtaining financing and consider taking more than you need while considering the premium it costs.

2) Increase your contract timeframe

This ties to the previous one. The longer you stay in a good setup, the longer you are exposed to upsides. And the downside too, so be sure to account for disaster scenarios; otherwise, you are just gambling.

Invest with insurance!

3) Negotiate great refinancing options

In investing, obtaining suitable financing is vital. To take advantage of this, your contract must be flexible enough. Times change, and if they change for the good, refinance your loan; if they change for the bad, enjoy the benefits.

4) Think twice about early repayment

This one is tricky. At first, it seems when you pay interest on something higher than the inflation, paying it back early is perfectly reasonable. It depends; I invite you to view this in a different light.

You have money at your disposal and must decide what to do with it. Think of loan repayment as an investment option. It has its yield and capital requirements. Alternative options also exist. Explore those thoroughly before deciding. Blindly repaying debt is plain dumb. Think before you act.

Closing

All of these are derived from inflation, the strongest force in the monetary system. Not counting ad-hoc shocks, of course. You probably never thought of it this way. I don’t blame you; this does not come naturally. And, as I said in the beginning, your intuitions deceive you when it comes to money. There simply isn’t anything else in the natural world that resembles the mechanics of money.

I want to leave you with a question to ponder.

Who absorbs the inflation loss? 🤨

The sheets used throughout this post are available here. Feel free to play with the numbers and check different scenarios.

Leave a Reply